Per latest, “The path of economic contraction continues to slow. GDP shrank 2.5% y/y In January 2016 versus a 3.5% y/y fall in December 2015. We expect the economy to shrink 2.1% y/y in 2016 if the crude price stays at USD31/bl on average, while we would expect expansion to happen if the oil price climbs to USD59/bl on average.”

Overall, Danske’s view is that supply side of growth equation is now close to / already in expansionary territory, while demand (and investment) sides are both still struggling.

Problem is, this imbalance should be leading to rapidly declining inflation. In part this is starting to show through. As noted by Danske team: “Inflation eased to 8.1% y/y in February, from 9.8% y/y in January, as prices already included the RUB devaluation and the high base effect is weighing on the CPI. We expect 2016 inflation to stay single digit, posting 8.1% y/y in December 2016.”

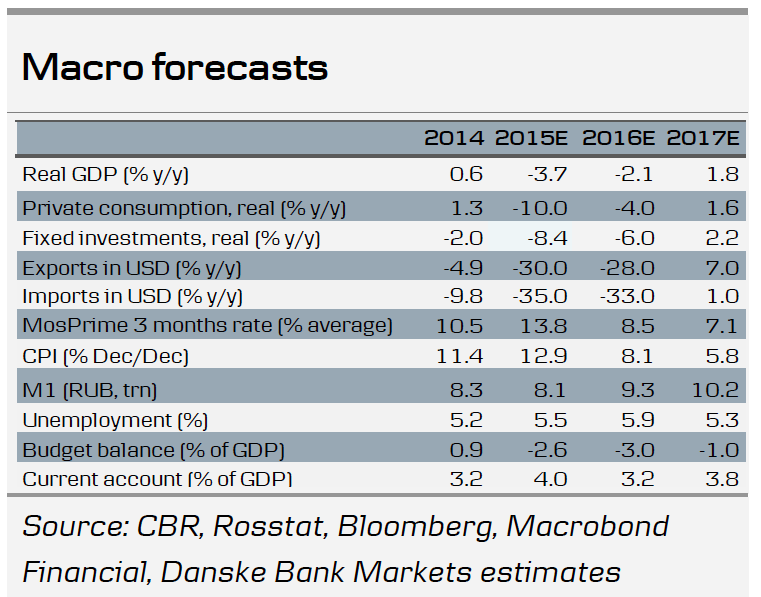

With this in mind, table below shows Danske’s forecasts summary

At -2.1% for 2016, this is a relatively moderate forecast, at the lower end of the forecast envelope for the consensus, but not low enough to raise eyebrows as with their 2015 outlook. CPI forecasts at 8.1% for 2016 is probably realistic, whilst 5.8% forecast for 2017 is quite likely to go unmet, given upside to growth penciled in and M1 expansion estimated at 9.3% and 10.2% in 2016-2017.

Overall, not that far off from my own expectations for the year, though Current Account surplus is, in my view, more likely to come in at around 3.5-3.8 percent of GDP.

The key to the above is the headline GDP figure (weak and likely to remain weak for some time into 2016) and external balances (strong and likely to remain such into 2016-2017). The economy is struggling to gain the elusive recovery footing, but it is also paying for itself.