Deutsche’s 6 percent perpetual bonds, CoCos (more on this below), with expected maturity in 2022, used to yield around 7 percent back in January. Having announced massive losses for fiscal year 2015 (first time full year losses were posted by the DB since 2008), Deutsche was under pressure in the equity markets. Rather gradual sell-off of shares in the bank from the start of 2015 was slowly, but noticeably eroding bank’s equity risk cushion. So markets started to get nervous of the second tier of ‘capital’ held by the bank – second in terms of priority of it being bailed in in the case of an adverse shock. This second tier is known as AT1 and it includes those CoCos.

Yields on CoCos rose and their value (price) fell. This further reduced Deutsche’s capital cushion and, more materially, triggered concerns that Deutsche will not be calling in 2022 bonds on time, thus rolling them over into longer maturity. Again, this increased losses on the bonds. These losses were further compounded by the market concerns that due to a host of legal and profit margins problems, Deutsche can suspend payments on CoCos coupons, if not in 2016, then in 2017 (again, more details on this below). Which meant that in markets view, shorter-term 2022 CoCos were at a risk of being converted into a longer-dated and zero coupon instrument. End of the game was: Coco’s prices fell from 93 cents to the Euro at the beginning of January, to 71-72 cents on the Euro on Monday this week.

When prices fall as much as Deutsche’s CoCos, investors panic and run for exit. Alas, dumping CoCos into the markets became a problem, exposing liquidity risks imbedded into CoCos structure. There are two reasons for the liquidity risk here: one is general market aversion to these instruments (a reversal of preferences yield-chasing strategies had for them before); and lack of market makers in CoCos (thin markets) because banks don’t like dealing in distressed assets of other banks. Worse, Asian markets were largely shut this week, limiting potential pool of buyers.

Spooked by shrinking valuations and falling liquidity of the Deutsche’s AT1 instruments, investors rushed into buying insurance against Deutsche’s default on senior bonds – the Credit Default Swaps or CDS. This propelled Deutsche’s CDS to their highest levels since the Global Financial Crisis. Deutsche’s CDS shot straight up and with their prices rising, implied probability of Deutsche’s default went through the roof, compounding markets panic.

Summing Up the Mess: Three Pillars of European Risks

Deutsche Bank AG is a massive, repeat – massive – banking behemoth. And the beast is in trouble.

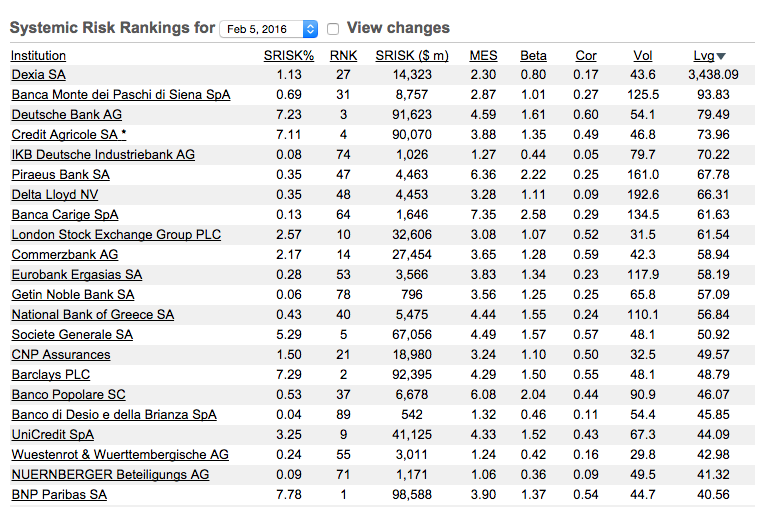

Let’s do some numbers first. Take a rather technical test of systemic risk exposures by the banks, run by NYU Stern VLab. First number of interest: Systemic Risk calculation – the value of bank equity at risk in a case of systemic crisis (basically – a metric of how much losses a bank can generate to its equity holders under a systemic risk scenario).

Deutsche clocks USD91.623 billion hole relating to estimated capital shortfall after the existent capital cushion is exhausted. A wallop that is the third largest in the world and accounts for 7.23% of the entire global banking system losses in a systemic crisis.

Now, for volatility that Deutsche can transmit to the markets were things to go pear shaped. How much of a daily drop in equity value of the Deutsche will occur if the aggregate market falls more than 2%. The metric for this is called Marginal Expected Shortfall or MES and Deutsche clocks in respectable 4.59, ranking it 8th in the world by impact. In a sense, MSE is a ‘tail event’ beta – stock beta for times of significant markets distress.

How closely does Deutsche move with the market over time, without focusing just on periods of significant markets turmoil? That would be bank’s beta, which is the covariance of its stock returns with the market return divided by variance of the market return. Deutsche’s beta is 1.61, which is high – it is 7th highest in the world and fourth highest amongst larger banks and financial institutions, and it basically means that for 1% move in the market, on average, Deutsche moves 1.6%.

But worse: Deutsche leverage is extreme. Save for Dexia and Banca Monte dei Paschi di Siena SpA, the two patently sick entities (one in a shutdown mode another hooked to a respirator), Deutsche is top of charts with leverage of 79.5:1.

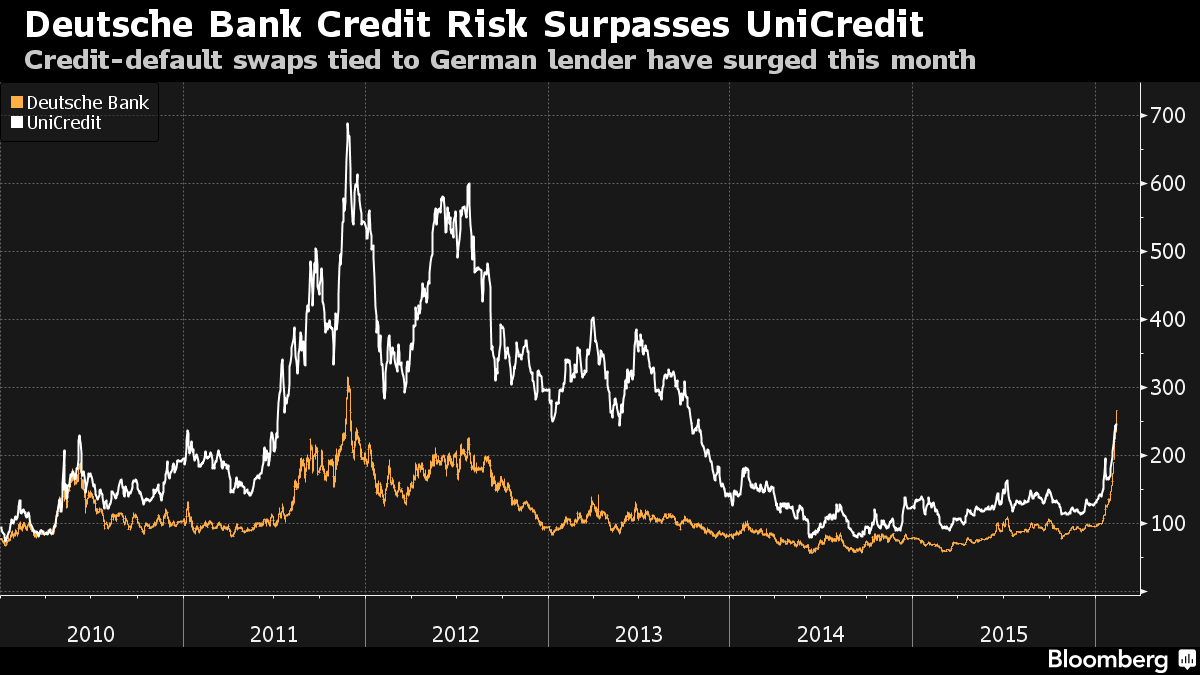

Incidentally, this week, Deutsche credit risk surpassed that of another Italian behemoth, UniCredit:

So Deutsche is loaded with the worst form of disease – leverage and it is caused by the worst sort of underlying assets: the impenetrable derivatives (see below on that).

Overall, Deutsche problems can be divided into 3 categories:

- Legal

- Capital, and

- Leverage and quality of assets.

These problems plague all European TBTF banks ever since the onset of the Global Financial Crisis. The legacy of horrific misspelling of products, mis-pricing of risks and markets distortions by which European banks stand is contrasted by the rhetoric emanating from European regulators about ‘reforms’, ‘repairs’ and ‘renewed regulatory vigilance’ in the sector. In truth, as Deutsche’s saga shows, capital buffers fixes, applied by European regulators, have yielded nothing more than an attempt to powder over the miasma of complex, derivatives-laden asset books and equally complex, risk-obscuring structure of new capital buffers. It also highlights just how big of a legal mess European banks are, courtesy of decades of their maltreatment of their clients and markets participants.

So let’s start churning through them one-by-one.

The Saudi Arabia of Legal Problems

Deutsche has been slow to wake up and smell the roses on all various legal settlements other banks signed up to in years past. Deutsche has settled or paid fines of some USD9.3 billion to-date (from the start of the Global Financial Crisis in 2008), covering:

- Charges of violations of the U.S. sanctions;

- Interest rates fixing charges; and

- Mortgages-Backed Securities (alleged) fraud with respect to the U.S. state-sponsored lenders: Fannie Mae and Freddie Mac.

And at the end of 2015, Deutsche has provided a set-aside funding for settling more of the same, to the tune of USD6 billion. So far, it faces:

- U.S. probe into Mortgages-Backed Securities it wrote and sold pre-crisis. If one goes by the Deutsche peers, the USD15.3 billion paid and set aside to-date is not going to be enough. For example, JP Morgan total cost of all settlements in the U.S. alone is in excess of USD23 billion. But Deutsche is a legal basket case compared to JPM-Chase. JPM, Bank of America and Citigroup paid around USD36 billion on their joint end. In January 2016, Goldman Sachs reached an agreement (in principle) with DofJustice to pay USD5.1 billion for same. Just this week (http://www.businessinsider.com/morgan-stanley-mortgage-backed-securities-settlement-2016-2) Morgan Stanley agreed to pay USD3.2 billion on the RMBS case. Some more details on this here: http://www.reuters.com/article/us-deutsche-bank-lawsuit-idUSKCN0VC2NY.

- Probes into currency manipulations and collusion on its trading desk (DB is the biggest global currency trader that is yet to settle with the U.S. DoJustice. In currency markets rigging settlement earlier, JPMorgan, Citicorp and four other financial institutions paid USD5.8 billion and entered guilty pleas already.

- Related to currency manipulations probe, DB is defending itself (along with 16 other financial institutions) in a massive law suit by pension funds and other investors. Deutsche says ‘nothing happened’. Nine out of the remaining 15 institutions are pushing to settle the civil suit for (at their end of things) USD2 billion. Keep in mind of all civil suit defendants – Deutsche is by far the largest dealer in currency markets.

- Probes in the U.S. and UK on its alleged or suspected role in channeling some USD10 billion of Russian money into the West;

- Worse, UK regulators are having a close watch on Deutsche Bank – in 2014, they placed it on the their “enhanced supervision” list, reserved for banks that have either gone through a systemic failure or are at a risk of such; a list that includes no other large banking institution on it, save for Deutsche.

- This is hardly an end to the Deutsche woes. Currently, it is among a group of financial institutions under the U.S. investigation into trading in the U.S. Treasury market, carried out by the Justice Department.

- The bank is also under inquiries covering alleged fixings of precious metals benchmarks.

- The bank is even facing some legal problems relating to its operations (in particular hiring practices) in Asia. And it is facing some trading-related legal challenges across a number of smaller markets, as exemplified by a recent case in Korea (http://business.asiaone.com/news/deutsche-bank-trader-sentenced-jail).

You really can’t make a case any stronger: Deutsche is a walking legal nightmare with unknown potential downside when it comes to legal charges, costs and settlements. More importantly, however, it is a legal nightmare not because regulators are becoming too zealous, but because, like other European banks, adjusting for its size, it has its paws in virtually every market-fixing scandal. The history of European banking to-date should teach us one lesson and one lesson only: in Europe, honest, functioning and efficient markets have been seconded to manipulated, dominated by TBTF institutions and outright rigged structures more reminiscent of business environment of the Italian South, than of Nordic ‘regulatory havens’.

CoCo Loco

CoCos, Contingent Convertible Capital Instruments, are a hybrid form of capital instruments that are designed and structured to absorb losses in times of stress by automatically converting into equity should a bank experience a decline in its capital ratios below a certain threshold. Because they are a form of convertible debt, they are counted as Tier 1 capital instrument ‘additional’ Tier 1 instruments or AT1.

CoCos are also perpetual bonds with no set maturity date. Banks can be redeemed them on option, usually after 5 years, but banks can also be prevented by the regulators from doing so. The expectation that banks will redeem these bonds creates expectation of their maturity for investors and this expectation is driven by the fact that CoCos are more expensive to issue for the banks, creating an incentive for them to redeem these instruments. European banks love CoCos, in contrast to the U.S. banks that issue preferred shares as their Tier 1 capital boosters, because Europeans simply love debt. Debt in any form. It gives banks funding without giving it a headache of accounting to larger pools of equity holders, and it gives them priority over other liabilities. AT1 is loved by European regulators, because it sits right below T1 (Tier 1) and provides more safety to senior bondholders on whose shoulders the entire scheme of European Ponzi finance (using Minsky’s terminology) rests.

In recent years, Deutsche, alongside other banks was raising capital. Last year, Credit Suisse, went to the markets to raise some CHF6 billion (USD6.1 billion), Standard Chartered Plc raised about $5.1 billion. Bank of America got USD5 billion from Warren Buffett in August 2014. So in May 2014, Deutsche was raising money, USD 1.5 billion worth, for the second time (it tapped markets in 2013 too). The fad of the day was to issue CoCos – Tier 1 securities, known as Contingent Convertible Bonds. All in, European banks have issued some EUR91 billion worth of this AT1 capital starting from 2013 on.

Things were hot in the markets then. Enticed by a 6% original coupon, investors gobbled up these CoCos to the tune of EUR3.5 billion (the issue cover was actually EUR25 billion, so the CoCos were in a roaring demand). Not surprising: in the world of low interest rates, say thanks to the Central Banks, banks were driving investors to take more and more risk in order to get paid.

There was, as always there is, a pesky little wrinkle. CoCos are convertible to equity (bad news in the case of a bank running into trouble), but they are also carrying a little clause in their prospectus. Under Compulsory Cancelation of Interest heading, paragraphs (a) and (b) of Prospectus imposed deferral of interest payments on CoCos whenever CoCos payment of interest “together with any additional Distributions… that are simultaneously planned or made or that have been made by the issuer on the other Tier 1 instruments… would exceed the Available Distributable Items…” and/or “if and to the extent that the competent supervisory authority orders that all or part of the relevant payment of interest be cancelled…”

That is Prospectus-Speak for saying that CoCos can suspend interest payments per clauses, before the capital adequacy problems arise. The risks of such an event are not covered by Credit Default Swaps (CDS) which cover default risk for senior bonds.

The reason for this clause is that European regulators impose on the banks what is known as CRD (Combined Buffer Requirement and Maximum Distributable Amount) limits: If the bank total buffers fall below the Combined Buffer Requirement, then CoCos and other similar instruments do not pay in full. That is normal and the risk of this should be fully priced in all banks’ CoCos. But for Deutsche, there is also a German legal requirement to impose an additional break on bank’s capital buffers depletion: a link between specified account (Available Distributable Items) balance and CoCos pay-out suspension. This ADI account condition is even more restrictive than what is allowed under CRD.

This week, DB said they have some EUR1 billion available in 2016 to pay on EUR350 million interest coupon due per CoCos (due date in April). But few are listening to DB’s pleas – CoCos were trading at around 75 cents in the euro mark this week. The problem is that the markets are panicked not just by the prospect of the accounting-linked suspension of coupon payments, but also by the rising probability of non-redemption of CoCos in the near future – a problem plaguing all financials.

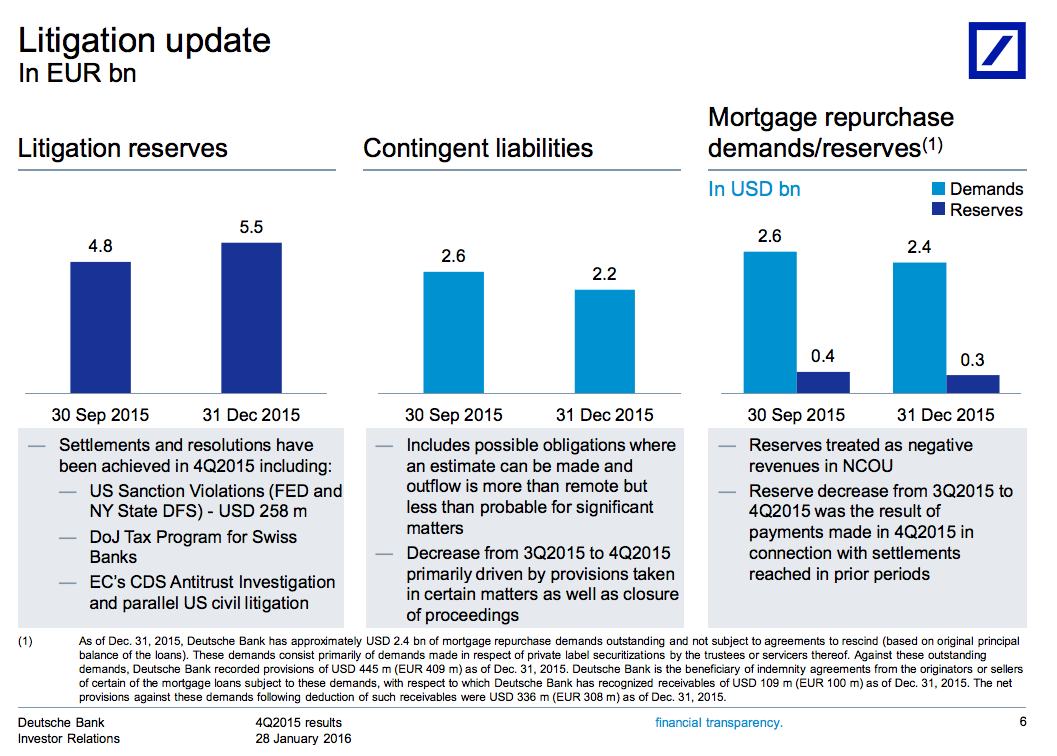

DB is at the forefront of these latter concerns, because of its legal problems and also because the bank is attempting to reshape its own business (the former problem covered above, the latter relates to the discussion below). DB just announced a massive EUR6.8 billion net loss for 2015 which is not doing any good to alleviate concerns about it’s ability to continue funding coupon payments into 2017. Unknown legal costs exposure of DB mean that DB-estimated expected funding capacity of some EUR4.3 billion in 2017 available to cover AT1 payments is based on its rather conservative expectation for 2016 legal costs and rather rosy expectations for 2016 income, including the one-off income from the 2015-agreed sale of its Chinese bank holdings.

Earlier this week, Standard & Poor’s, cut DB’s capital ratings on “concerns that Germany’s biggest lender could report a loss that would restrict its ability to pay on the obligations”. S&P cut DB’s Tier 1 securities from BB- to B+ from BB- and slashed perpetual Tier 2 instruments from BB to BB-.

Beyond all of this mess, Deutsche is subject to the heightened uncertainty as to the requirements for capital buffers forward – something that European banks co-share. AT 1 stuff, as highlighted above, is one thing. But broader core Tier 1 ratio in 4Q 2015 was 11.1%, which is down on 11.5% in 4Q 2014. In its note cutting CoCos rating, S&P said that “The bank’s final Tier 1 interest payment capacity for 2017 will depend on its actual net earnings in 2016 as well as movements in other reserves.” Which is like saying: “Look, things might work out just fine. But we have no visibility of how probable this outcome is.” Not assuring…

DB is also suffering the knock-on effect of the general gloom in the European debt markets. Based on Bloomberg data, high yield corporate bonds issuance in Europe is down some 78 percent in recent months, judging by underwriters fees. These woes relate to European banks outlook for 2016, which links to growth concerns, net interest margin concerns and quality of assets concerns.

Badsky Loansky: A Eurotown’s Bad Bear?

Equity and debt markets repricing of Deutsche paper is in line with a generally gloomy sentiment when it comes to European banks.

The core reason is that aided by the ECB’s QE, the banks have been slow cleaning their acts when it comes to bad loans and poor quality assets. European Banking Authority estimates that European banks hold some USD 1.12 trillion worth of bad loans on their books. These primarily relate to the pre-crisis lending. But, beyond this mountain of bad debt, we have no idea how many loans are marginal, including newly issued loans and rolled over credit. How much of the current credit pool is sustained by low interest rates and is only awaiting some adverse shock to send the whole system into a tailspin? Such a shock might be borrowers’ exposures to the US dollar credit, or it might be companies exposure to global growth environment, or it might be China unwinding, or all three. Not knowing is not helpful. Oil price collapse, for example, is hitting hard crude producers. Guess who were the banks’ favourite customers for jumbo-sized corporate loans in recent years (when oil was above USD50pb)? And guess why would any one be surprised that with global credit markets being in a turmoil, Deutsche’s fixed income (debt) business would be performing badly?

Deutsche and other european banks are caught in a dilemma. Low rates on loans and negative yields on Government bonds are hammering their profit margins (based on net interest margin – the difference between their lending rate and their cost of raising funds). Solution would be to raise rates on loans. But doing so risks sending into insolvency and default their marginal borrowers. Meanwhile, the pool of such marginal borrowers is expanding with every drop in oil prices and every adverse news from economic growth front. So the magic potion of QE is now delivering more toxicity to the system than good, and yet, the system requires the potion to flow on to sustain itself.

Again, this calls in Minsky: his Ponzi finance thesis that postulates that viability of leveraged financial system can only be sustained by rising capital valuations. When capital valuations stop growing faster than the cost of funding, the system collapses.

In part to address the market sentiment, Deutsche is talking about deploying the oldest trick in the book: buying out some of its liabilities – err… senior bonds (not CoCos) – at a discount in the markets to the tune of EUR5 billion across two programmes. If it does, it will hit own liquidity in the short run, but it will also (probably or possibly) book a profit and improve its balance sheet in the longer term. The benefits are in the future, and the only dividend hoped-for today is a signalling value of a bank using cash to buy out debt. Which hinges on the return of the markets to some sort of the ‘normal’ (read: renewed optimism). Update: here’s the latest on the subject via Bloomberg http://www.bloomberg.com/news/articles/2016-02-12/deutsche-bank-to-buy-back-5-4-billion-bonds-in-euros-dollars

Back to the performance to-date, however.

Deutsche Bank’s share price literally fell off the cliff at the start of this week, falling 10 percent on Monday and hitting its lowest level since 1984.

On bank’s performance side, concerns are justified. As I noted earlier, Deutsche posted a massive EUR6.89 billion loss for the year, with EUR2 billion of this booked in 4Q alone. Compared to 2014, Deutsche ended 2015 with its core equity Tier 1 capital (the main buffer against shocks) down from EUR60 billion to EUR52 billion.

Still, panic selling pushed DB equity valuation to EUR19 billion, in effect implying that some 2/3rds of the book of its assets are impaired. Which is nonsense. Things might be not too good, but they aren’t that bad today. The real worry with assets side of the DB is not so much current performance, but forward outlook. And here we have little visibility, precisely because of the utterly abnormal conditions the banks are operating in, courtesy of the global economy and central banks.

So markets are exaggerating the risks, for now. Psychologically, this is just a case of panic.

But panic today might be a precursor to the future. More of a longer term concern is DB’s exposure to the opaque world of derivatives that left markets analysts a bit worried (to put things mildly). Deutsche has taken on some pretty complex derivative plays in recent years in order to offset some of its losses relating to legal troubles. These instruments can be quite sensitive to falling interest rates. Smelling the rat, current leadership attempted to reduce bank’s risk loads from derivatives trade, but at of the end of 2015, the bank still has an estimated EUR1.4 trillion exposure to these instruments. Only about a third of the DB’s balance sheet is held in German mortgages and corporate loans (relatively safer assets), with another third composed of derivatives and ‘other’ exposures (where ‘other’ really signals ‘we don’t quite feel like telling you’ rather than ‘alternative assets classes’). For these, the bank has some EUR215 billion worth of ‘officially’ liquid assets – a cushion that might look solid, but has not been tested in a sell-off.

In summary:

Deutsche’s immediate problems are manageable and the bank will most likely pull out of the current mess, bruised, but alive. But the two horsemen of a financial apocalypse that became visible in the Deutsche’s performance in recent weeks are worrying:

1) We have a serious problem with leverage remaining in the system, underlying dubious quality of assets and capital held and non-transparent balance sheets when it comes to derivatives exposures; and

2) We have a massive problem of residual, unresolved issues arising from incomplete response to markets abuses that took place before, during and after the crisis.

And there are plenty potential triggers ahead to derail the whole system. Which means that whilst Deutsche is not Europe’s Lehman, it might become Europe’s Bear Sterns, unless some other TBTF preempts its run for the title… And there is no shortage of candidates in waiting…

Links:

DB’s 2015 report presentation deck: https://www.db.com/ir/en/download/Deutsche_Bank_4Q2015_results.pdf

DB’s internal memo to employees on how “ok” things are: https://www.db.com/newsroom_news/2016/ghp/a-message-from-john-cryan-to-deutsche-bank-employees-0902-en-11392.htm