This is an unedited version of my article for Manning Financial. Final version is available here:

In almost every sharp downshift in economic activity, and more frequently than that, in almost every economic recession, there are several regular predictors or leading indicators of tougher times ahead. These include sharp drops in corporate profits, and acceleration in yields on lower rated corporate bonds, usually followed by significant declines in industrial production indices and subsequent downward corrections in stock markets and services activities indices.

While these sequences of events repeat with regularity, in many cases, forward signals of recessions can involve a slight variation in timing and permutations of these shocks.

Another regularity that happens when it comes to business cycles is that, traditionally, the U.S. leads Europe into the downturn.

Trouble is, judging by all factors mentioned above, the U.S. is currently heading into a recession. Fast. And with some vengeance.

The Bad News

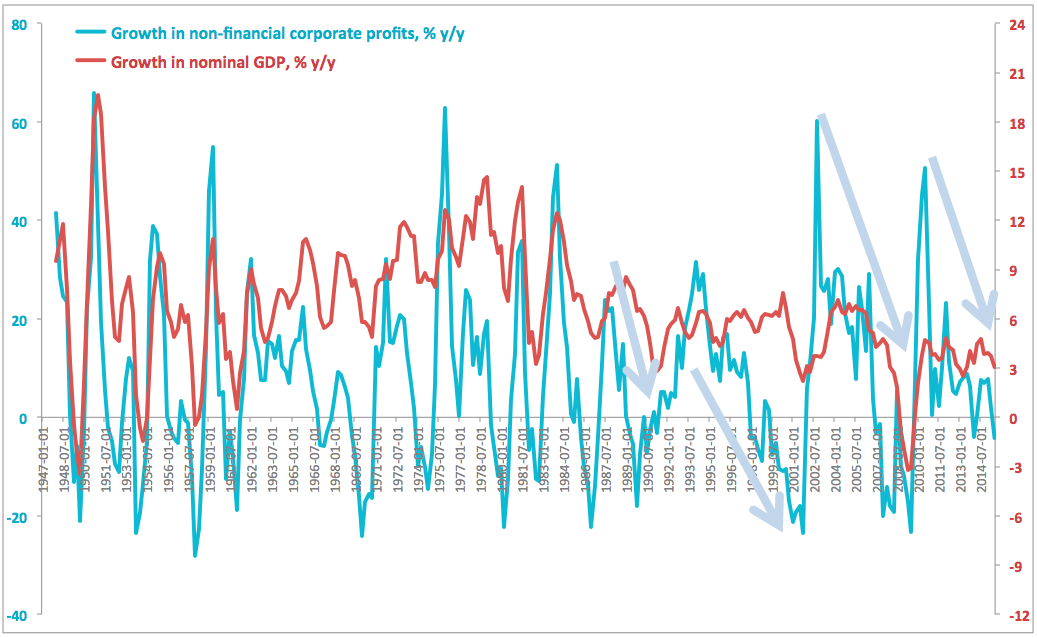

Let’s start with corporate profits. The latest data from the U.S. Federal Reserve shows that year-on-year 3Q 2015 growth in corporate profits for non-financial corporations was sharply negative – at -4.26 percent. Furthermore, corporate profits growth slowed down from 7.72 percent in 1Q 2015 to 1.83 percent in 2Q 2015. The rate of decline in corporate profits growth in the U.S. is now sharper than during the last GDP wobble in 1Q 2014 and sharper than in 3Q 2008. The latest growth figure also marks the fastest rate of decline in profits since 3Q 2009.

CHART 1: Non-Financial Corporate Profits and Nominal GDP

Growth Rates, Percent per annum

Source: Author own calculations based on data from the Federal Reserve Bank

Chart above shows clear pattern of correlation between corporate profits growth rates and subsequent growth rate in nominal GDP. It also shows that U.S. corporate profits growth rates have been on a declining trend since 3Q 2010.

Meanwhile, corporate debt yields are shooting straight up. Added to this dynamic is another troublesome sign: yields volatility is also on the rise. In other words, the markets are not only nervous about individual issuers, but are appearing to be scared of the entire asset class. I wrote about this phenomena in previous newsletter, here. Behaviourally, international and U.S. investors have been running for the hills for some time now, despite the extremely risk-supportive monetary policies not just by the Fed, but also by major carry trade-sustaining central banks (Bank of Japan and ECB). In normal conditions, carry trade drivers should moderate risk aversion effects. Except they are not doing so today.

As noted in a recent research note by J.P. Morgan Cazenove in general, credit spreads lead equities and the former “are not giving a positive signal” to the latter (see: http://trueeconomics.blogspot.com/2016/01/24116-high-yield-bonds-flash-red-for.html).

So that puts two recession-beaconing stars into a perfect alignment.

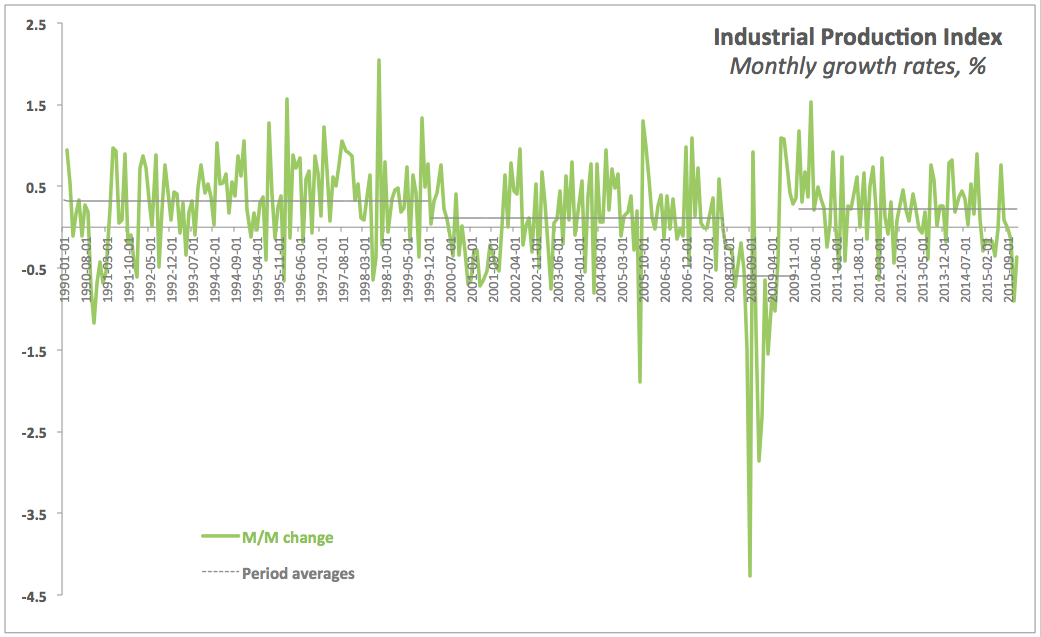

What about the U.S. Industrial Production? From over 2015, U.S. industrial output posted declines, based on monthly growth rates, in ten months out of twelve, with December 2015 production levels down almost 2 percent on December 2014 peak. In annual growth terms, output growth rate started at a brisk 4.48 percent pace in January 2015 and ended the year with a contraction of 1.75 percent – the sharpest rate of decline since December 2009. That’s a swing of some 6.23 percentage points in 12 months.

CHART 2: U.S. Industrial Production Index

Monthly growth rates, percent

Source: Author own calculations based on data from the Federal Reserve Bank

Like with corporate bonds and profits, some of this is down to a combination of commodities recession and Emerging Markets woes.

The former is pretty apparent to all concerned. Between the start of 2014 and the end of 2015, the weighted average price of oil across three key grades (Brent, WTI and Fateh) fell 51.1 percent. Non-fuel commodities went down 21 percent.

The latter also was subject to my earlier contributions to this newsletter. To update you with the latest news, while Emerging Markets continued to contribute some 70 percent of overall global growth in 2015, the rate of growth in key BRICS economies (including Brazil, Russia, India, China and South Africa) has been tanking.Per latest IMF forecasts, released earlier this month, Emerging Markets are still expected to grow by 4.3 and 4.7 percent in 2016 and 2017. However, this puts their growth rates below the 2011-2014 average of 5.3 percent and the 2000-2007 average of 6.5 percent. Amongst the BRICS, all but China and India are either already in a recession or one quarter away from a recession. China is expected to post official growth of 6.9 percent in 2015, with forecast for 2016-2017 for 6.3 percent and 6.0 percent, respectively. Even if trust Chinese official statistics, this represents a big drop. For example, 2015 has been the slowest year in terms of GDP growth in 25 years, and the fourth slowest in 36 years.

But beyond these two factors, U.S. output growth is also being pushed down by stronger Dollar and collapsing global trade. Global trade has been tracking the declining fortunes of global demand since 2012. Over the last four years, global trade volumes growth underperformed post-crisis average and historical average, pushing growth rates to their lowest readings for any decade on record. In line with this, Baltic Dry Index – the cost indicator for hiring cargo vessels to ship goods around the world – has been hitting historical lows almost on a daily basis since the second part of December 2015.

All of the above factors, from falling profits, to falling production growth rates, to underlying commodities recession, global demand weaknesses and international currencies re-valuations, have undoubtedly contributed to falling equity prices. Since the start of 2016, some forty major equity markets around the world have entered bear territory. While on the corporate side of the U.S. economy, oil and commodities prices recession has been a dominant driver for aggregate equities indices movements, underlying equity price swings are much broader currents. For example, equities sell-offs around the world did not concentrate on commodities producing sectors and companies, or on highly leveraged corporates alone. Instead, the bear markets have been broad.

The Good News

Which brings us to last piece of a puzzle, yet to fall into its place: consumer demand. Or put into the above context – the good news bit.

Falling equity and bond prices, as well as rising retail interest rates are capable of triggering – if sustained over time – drops in consumer confidence, followed by households’ pulling back from consumption and investment. So far, stronger dollar (improving U.S. consumers’ purchasing power), lower energy prices (improving their disposable incomes) and falling unemployment (improving household pre-tax incomes) have sustained consumer confidence at healthy levels.

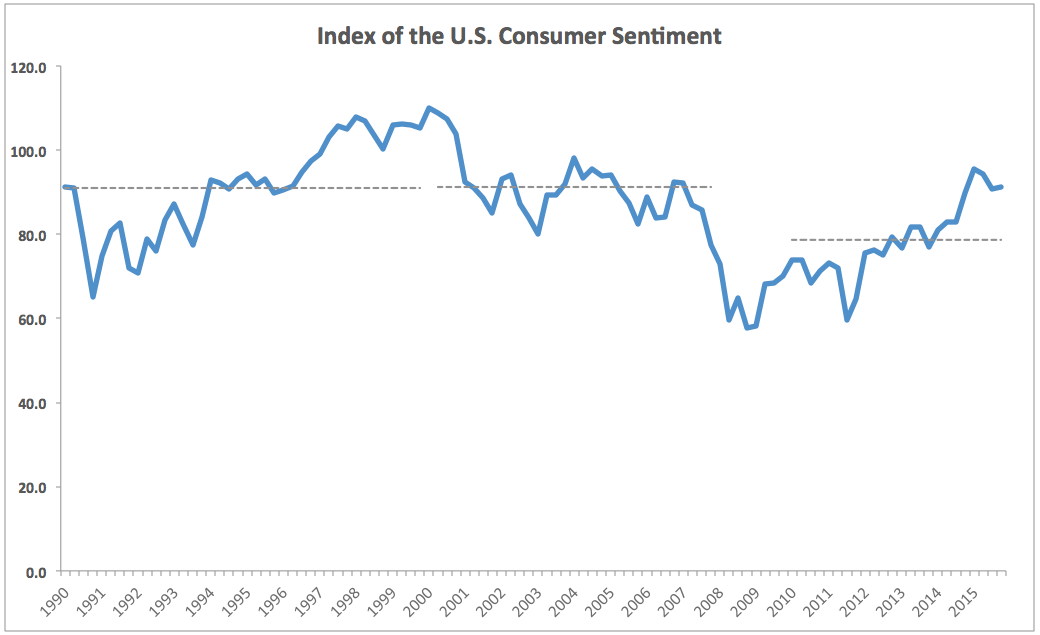

CHART 3: Index of the U.S. Consumer Sentiment

Source: University of Michigan

However, current levels of consumer confidence are barely touching pre-crisis averages and have declined since local peak in January 2015 through 3Q 2015. There is no crisis at the moment, but given the strength of household finances, 2015 index performance was hardly spectacular.

Whatever resilience we do see in consumer surveys, it is most likely underpinned by the positive jobs prints. Based on historical figures, over each recessionary episode in the U.S. history since the end of the World War II, employment was one of the key casualties, declining with every recession by at least 1 percentage point. U.S. added 2.597 million new private sector jobs over the course of 2015 and average weekly earnings are rising in both goods-producing and services-providing sectors.

The Latest Official Forecasts

This is precisely why despite the leading indicators flashing bright warning signs of the potential incoming recession, the IMF continues to forecast rather robust – by comparatives to the Euro area, UK and Japan – for the U.S. in 2016 and 2017. Per January update to its forecasts, the IMF now expects U.S. economy to grow at 2.6 percent in both 2016 and 2017. This comes against the Fund forecast for 2.2 percent growth in 2016 and 2017 in the UK, 1.7 percent real growth in the Euro area over the same period, and 1 percent and 0.3 percent growth in Japan in 2016 and 2017, respectively. However, IMF’s latest forecast represents a sizable downgrade for the U.S. compared to previous forecasts. Thus, compared to October 2015 outlook, IMF expectations for U.S. economic expansion are now 0.2 percentages lower for both 2016 and 2017.

Still, IMF references the U.S. as one of the four core risks to its global outlook for 2016. Specifically, the IMF cites the risk arising from “tighter global financing conditions as the United States exits from extraordinarily accommodative monetary policy”.

This risk, along side growing uncertainty about overall health of the U.S. economy, are material factors for Irish and European markets and investors. Ireland benefited significantly from the U.S. recovery and subsequent devaluation of the Euro vis-à-vis the U.S. dollar. These factors underpinned our exports of goods to the U.S. and Canada rising by EUR6.85 billion for the first eleven months of 2015 compared to the same period in 2012. This growth is more than double the rate of expansion in our trade in goods with the EU (including the UK). From Irish investors perspective, our domestic assets performance – across both equities and bonds – owes a lot to the resilience of the U.S. economy. Likewise, our investors’ access to diversified portfolios of internationally-listed and traded assets cannot be imagined absent the U.S. equity and debt markets.

All of this is currently at risk when it comes to the U.S. economic and markets performance forward. And more ominously, our own European economic and investment fortunes are tied closely to the North American economies. Whenever you hear any political leader – be it Enda Kenny or Jean-Claude Juncker – extoling the virtues of Ireland’s or Europe’s firewalls against international shocks, remember the old adage: when America sneezes, Europe catches the cold.