Remember record-busting 0.6% preliminary flash estimate of the first estimate GDP growth figure for Euro area released back in April? Well, it sort of was true, sort of…

Eurostat now puts 1Q 2016 growth at 0.5% q/q in its updated estimate released today – 0.1% lower than the April estimate. This figure is tied jointly for highest q/q growth figure since 1Q 2011 when it hit 0.8%.

Sounds good? Brilliant – the euro area outperformed both the U.S. and the UK. But when one looks at annual rates of growth… things are not as shiny.

There is a strong smell of smoke from the Eurostat figures. Demand side of the economy is apparently booming. Despite the fact that retail sales are tanking:

Meanwhile, external trade is also underperforming (on foot of euro appreciation from November 2015 lows against both the US dollar and British pound):

Euro bottomed out at around 1.057 to the dollar at the end of November, and steadily gained against the USD every month since, with current valuation around 1.13-1.14 range. This hardly supports European exports to the U.S. Controlling for volatility, similar trend is against British Pound. About the only thing going the euro way today is yen and it is immaterial to the Euro area’s economy.

So euro zone economic growth appears to be loosing momentum since the start of 2Q 2016. And there are both short term drivers for this and long term ones.

Short term drivers, as outlined above suggest that current risks environment appears to be titled to the downside:

- Eurozone Composite Output Index by Markit posted 53.0 in April against March 53.1. Statistically-speaking, the rate of growth effectively remained static.

- German Composite PMI was at 53.6, which is an 11-months low, French Composite index reading was 50.2 (barely above the 50.0 line, but still at 3mo high), while Italian Composite PMI in April came in at 53.1, also 2 months high.

- Importantly, the euro zone PMI indices have been moving out of step with the Global PMI readings. In April, while eurozone PMI declined marginally compered to the end of 1Q 2016, Global PMI reading marginally picked up, rising from 51.5 in March to 51.6 in April.

- The ongoing stagnation in France continued, while solid expansions were noted in Germany, Italy, Spain and Ireland.

- Developed markets saw all-industry output rise at the fastest pace in three months during April. However, the rate of increase still one of the weakest registered during the past three years. Growth remained only modest in both the US and the UK (UK growth slowed to its weakest pace since March 2013). This puts pressure on demand for eurozone exports and, in turn, pressures profit margins and investment.

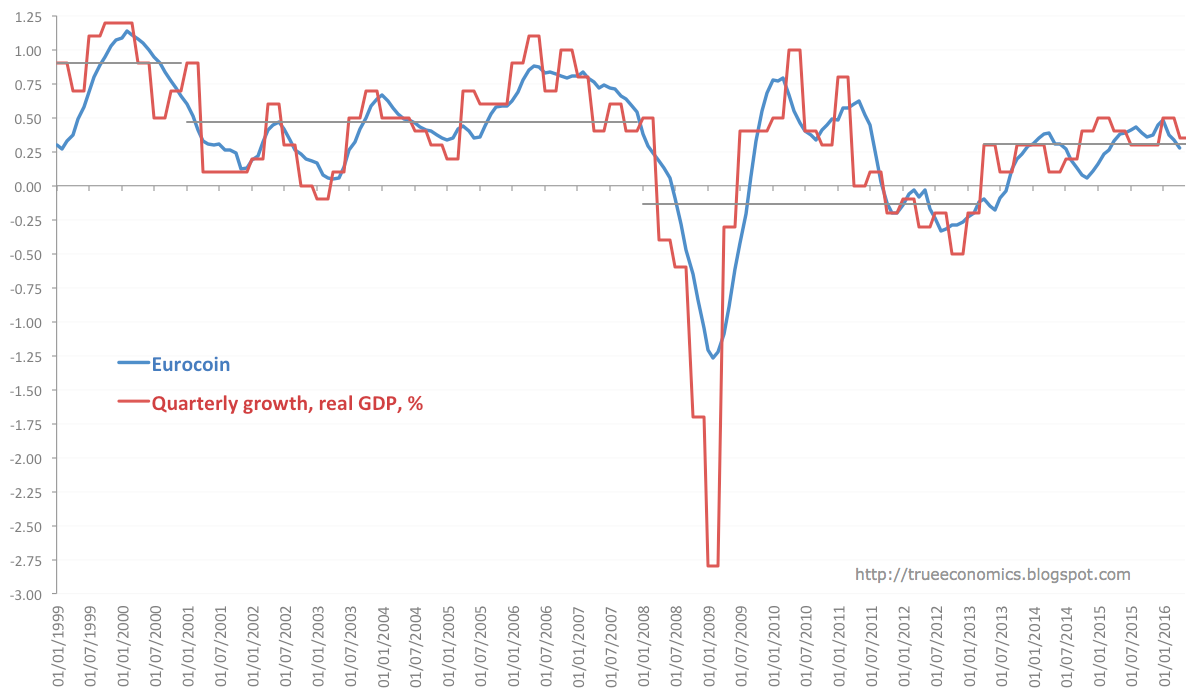

- Given 1Q growth estimate at 0.5% (q/q growth) from the Eurostat, current level of Eurocoin suggest quarterly growth slowdown to around 0.4%.

- Ifo’s Economic climate indicator for the Euro area has now been on a clear declining trend since mid-2015 and is now at its lowest levels since 1Q 2015 and second lowest reading in two-and-a-half years.

- In Germany, consensus estimates put gross domestic product growth at 0.3 percent in the current quarter and 0.4 percent in 3Q and 4Q, with full year growth of around 1.5 percent.

My view: we might see 2Q growth coming in at 0.3-0.4 percent, if April trends continue into the rest of 2Q. Overall, I expect 2016 growth to be around 1.4-1.5 percent which is just about to the downside on current consensus estimate of 1.5 percent.

Long term drivers for structural euro zone growth weakness: Even with positive 1Q 2016 print on growth side, it is fairly clear that euro zone lacks serious growth catalysts.

Everyone is talking about Brexit referendum and the renewal of the Greek crisis as key threats. Put frankly – this is a smokescreen. When it comes to longer term euro zone growth prospects both are irrelevant. Growth within the euro area has nothing to do with the UK. And Greece has been effectively removed from the markets and economic agents’ considerations – the country is no longer commanding any serious media attention (with markets fatigued by the never-ending ‘crises’). With ESM / EFSF /ECB now seemingly the sole bearers of Greek debt (with IMF likely to take back seat in the Bailout 3.0 as per http://trueeconomics.blogspot.com/2016/05/11516-71-steps-guide-to-greek-crisis.html) Greek funding issues and any risk of a default are unlikely to trigger Grexit. Put more directly, even if Greece were to exit the Euro, no one will bat an eyelid over such an event.

Meanwhile, the real long term problems for the euro area are:

- Capex remains subdued across the entire euro area, including Germany, Italy, France.

- Fiscal policy is currently largely neutral and it is hard to see how the euro area can find any significant capacity to increase fiscal spending.

- ECB stimulus is working in the financial markets, but not on the ground – there is still too much debt and too little prospect for a return on capital. Quality borrowers are not rushing to take on loans for capex. And the banks are not too eager to lend to borrowers with legacy leverage problems.

- Eurozone banking is still a mess: capital and loans restructuring is sporadic, rather than systematic, negative rates taking a bite out of margins, but even if this headwind is taken out, markets volatility is not helping.

And there are even bigger structural headwinds:

- Lack of agility in the structurally over-regulated and sclerotic economy: technological innovation is weak, adoption of technological innovation is weak, labour force quality is deteriorating, so productivity growth has collapsed. Entrepreneurship is weak. Employment is sluggish and of deteriorating quality. That’s supply side.

- Demand side is improving due to a short term boost from the post-Great Recession cyclical recovery. But, legacy issues of debt across corporate and household sectors and public finances are still present.

- On financial side: banks-intermediated funding model for capex is a drag on growth and there is zero momentum on equity and direct debt issuance sides. Even with ECB going into another round of TLTROs, issuance of new bonds has spiked primarily because of larger corporates issuance, not because of market deepening.

- On policies front, there is total and comprehensive paralysis. EU is malfunctioning, torn apart by crises of European making. National governments have lost capacity to legislate because of delegation of so much decision making to Brussels in the past. Political discontent is rising everywhere. We now have growing proportions of core European countries’ populations – the Big 4s – wanting to reexamine the entire EU.

Europe has been Japanified. And there is little that it can do to avoid this stagnation trap. There is no hope that fiscal policy can do what monetary policy has failed to deliver – the great hope of Keynesianistas. And with that, both the monetary and the fiscal sides of European growth equation are out. What’s left? Endless low interest rates (with a risk of policy error, should Germans rebel against Draghi’s uncountable puts) and endless painful quasi-deflating (through low demand) of debt. Aka, pain.